2019 Q1 Newsletter

"Things can only get better

Can only get, can only get

They get on from here

You know, I know that

Things can only get better"

D:Ream 1993

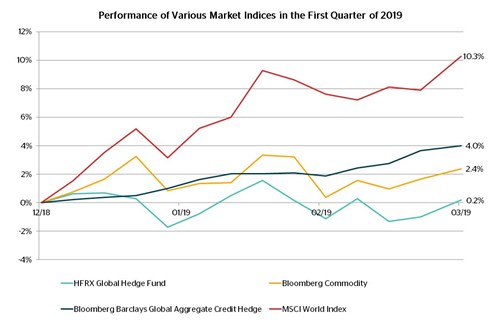

We concluded 2018 with “nowhere to run baby, nowhere to hide” by Martha and the Vandellas. The reason for this was that in the last quarter of 2018, all asset classes fell in value: there seemed to be no respite. Yet, here we are a mere three months later and the reverse is true – it has been difficult not to make money in Q1 as all asset classes have risen. Perhaps “things can only get better” would have been more appropriate at Christmas…

On the other side of the pond, Trump continues to wage trade wars and tweet his every move. That said, following the publication of the Mueller

report he has had the cloud of collusion between his campaign and the Russians lifted for now at least. This is good news for US politics and great news for The Donald – however, I don’t imagine for a minute that following this announcement we will experience a more calm, quiet and measured President Trump.

As I write, Theresa May is about to make a statement to the Commons. Surely not another “vote for my deal or it’s curtains” (at the third time of asking)? Will we end up without a deal simply because of the incompetence of both negotiating parties? Or will we, farcically, be compelled to vote again in the European Elections in June for an institution we have already voted to leave? You couldn’t make this stuff up – and a stuff-up is precisely what it has become. Funnily enough, “Things Can Only Get Better” lyrics were adopted by Labour as the anthem to their 1997 election campaign. From this current low point, the state of British politics must surely improve – the UK has been sorely let down by its politicians with both of the UK’s largest parties failing to deliver on their manifestos. But where does all of this leave us?

We would say that we’re where we always find ourselves, unable to predict or forecast short-term political or economic outcomes, never mind the vagaries of the market. Who knows whether things will get better soon? I would suggest most of us resident in the UK (or, at least, nearby!) will be delighted when the Brexit torture is over. Nevertheless, the void will no doubt quickly be filled by the next political or economic drama; it always is.

It is for this very reason (well, one of them) that the investment team invests both globally and thematically. By doing so it is possible to mitigate much of the idiosyncrasy associated with those political and economic risks specific to geographical regions.

Our themes will remain valid no matter whether the UK ends up with a hard BREXIT, a delayed BREXIT, no BREXIT or…(please, no!) perpetual BREXIT.

Source: Financial Express 2019. Data is GBP total return.

Cautious Portfolios:

Lower Risk

by Bob Tannahill

Objective: The Cautious Portfolio’s objective is to increase its value by predominantly allocating capital to fixed-income investments. The portfolio can also invest into global blue-chip equities with strong cash-flows and progressive dividend policies. A neutral position would be a 75% bond/25% equity split and the maximum equity-weighting of approximately 35%. The cash generated can be re-invested to provide capital or taken as an income stream.

The first three months of 2019 certainly set a very different tone to that of the end of 2018, with the Strategy returning around 4.5% – more than reversing the negative return posted for the previous year. The stock market blip troughed around the year-end and a large part of the gains seen in the first three months of this year is attributable to market bounce, as well as alleviated tension in the US-China trade discussions and the Federal Reserve signalling an end to its rate-hiking intentions for the time being.

The bounce has returned the market to its previous state where equities are again relatively expensive compared to their long-term history.

Consequently, we continue to maintain a constructive-but-cautious stance, which means a 25% equity and 75% bond split in the portfolio.

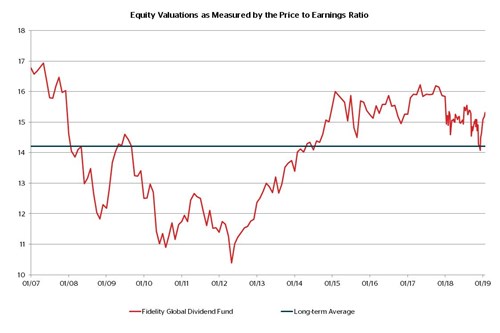

We did look at the potential for topping-up our equity exposure on valuation grounds, but did not find clear-cut value to justify it. The price/earnings graph for the Fidelity Global Dividend Fund (below) shows the drop in valuations around the year-end. Looking over the longer term from a qualitative perspective, valuations got close to what we could call fair value, but didn’t break through the line sufficiently for us to take the decision. When mixed with caution around corporate earnings indicating a potential peak associated with the latter stages of the business cycle, all this meant that we didn’t pull the trigger.

A deeper look at how the components of the portfolio performed over the quarter shows that all of the underlying funds performed positively. The best were the equity funds rallying on the back of strong market performance and it was pleasing to see that all three of our global equity income funds beat the sector average.

On the bond side of the portfolio, the top performers were those funds with more credit risk: high yield then corporate bonds. Following these

were the gilts and short-dated corporate bond funds – all in-line and behaving as we would expect in this sort of market environment.

A fund we specifically wanted to comment on at the quarter end is the Muzinich Asia Credit Fund. This has performed well and, more importantly, has behaved as we would have wanted it to over the past six months, i.e. differently to the other corporate bond funds that have exposure to the more established bond markets. We added this fund to the portfolio to add diversification and broaden our geographic exposure; it has done the job admirably.

Finally, to address the swathes of recent market commentary around yield-curve inversions and recession indications, in the first instance, it’s important to remember that there have been many more yield-curve inversions than there have been recessions. While we would not deny that an inverted yield curve is a significant development, as it implies investors believe the next step for the Fed will be to cut interest rates, we would not recommend relying on it too heavily. While inversions have preceded market falls they have also been followed by rallies and at other times it has taken a number of years between the initial inversion and the eventual downturn.

In addition to this, we are yet to see a decisive inversion in this cycle with the yield curve having un-inverted again at the time of writing. So our take on this development is that it adds to a number of issues, such as cyclically high margins and high corporate debt levels that have led to our “proceed with caution” mantra. This means we want to see clear value in assets before we top up any positions and that is why we sat on our hands over the year-end neither adding nor cutting our positions.

At the same time we are not simply waiting for markets to get cheaper in general. The team are working hard to scour our investable universe for any undiscovered pockets of opportunity and to help future proof the portfolio.

We haven’t found anything quite yet but, as we have mentioned a few times recently, we have a number of irons in the fire on this front.

More on that with any luck next quarter.

Balanced Portfolios:

Medium Risk

by Tiffany Gervaise-Brazier

Objective: The Balanced Portfolio’s objective is to provide capital appreciation through a balance of fixed income and global equities. A neutral position is a 50% bond/50% equity split and the maximum equity weighting is 60%. The cash generated can be re-invested to provide capital or taken as an income stream.

Thus far in 2019 we have seen both bonds and equities surge: bouncing back from the late-2018 sell-off sparked by fears of downbeat global

economic data, political turmoil and monetary policy normalisation. As a result, the Strategy has returned approximately 6% year-to-date. Whilst this is a pleasing return over a short space of time, it is too early to sound the all-clear signal.

Without wanting to sound pessimistic, we cannot see that much has changed. The reason for this is that our investment decisions are founded on stock and fund valuations; yet, and despite the sell-off, these are now back to trading at heightened valuations. Nonetheless, the recent market correction and rebound has provided us with the opportunity to re-balance the portfolio back to a 50:50 allocation of bonds to equities.

Further, we have made the decision to trim and take profit from our global equity allocation on valuation grounds; this reduction has been taken from our holding in the Lindsell Train Global Equity Fund. In terms of performance, the Fund is currently up over 20% from this time a year ago and up over 10% in the first quarter of the year.

Whilst we remain confident in the longevity of these returns from its managers over the long term, we nevertheless consider it prudent to trim the position from 9% to 7.5%, based on its current valuation.

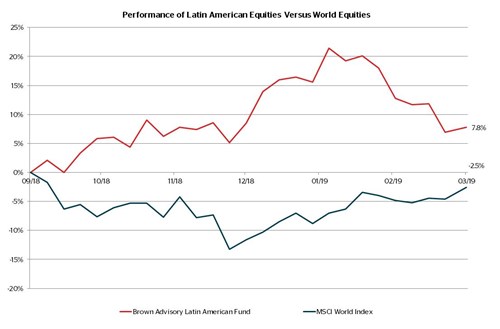

In an attempt to avoid talking about BREXIT (too much), elsewhere in the portfolio we are pleased to see that our emerging-market exposure, held through the Brown Advisory Latin American Fund, has had a strong few months following a torrid 2018. Not only do we believe in the tailwind for growth that the region will provide over the long term, we like the relatively uncorrelated performance of the Fund (as seen below) compared to developed market equities. In addition, the emerging market allocation gives us exposure to the more cyclical sectors, which we feel is no bad thing given the volatility that we have been facing of late.

Currently, with the portfolio in its most defensive position since inception, we want to retain stock and bond exposures that will provide long-term growth if the upward trend continues.

However, if markets begin to be troubled, the current portfolio allocation of the Strategy should protect on the downside and allow for a slightly smoother journey to achieving long-term capital growth for our clients.

Inevitably, BREXIT is weighing on investors’ minds and whilst it may feel like a purely domestic political issue, it certainly isn’t the only political volcano rumbling – it just might be the first to erupt. There is an array of global political and economic issues that could impact markets which, for the moment, remain dormant: Chinese debt-to-GDP ratios, trade wars and European recessions, to name but a few.

Whilst invested in capital markets – and the Strategy has 50% of its portfolio invested into global equities – it is important to note that one is never “BREXIT-proof” or “Trump-proof”, since we simply cannot forecast what will happen. However, one reassurance we can offer clients is that we continue to invest their hard-earned assets in high-quality, liquid investments at sensible valuations – and then rigorously monitor them in order to ensure that they stand the test of time.

Growth Portfolios:

Higher Risk

by Samantha Dovey

Objective: The Growth Portfolio’s objective is to provide long-term capital appreciation by investing predominantly into global equities. A neutral position is a 25% bond/75% equity split and the maximum equity weighting is approximately 85%.

The Dichotomy of 2018 and 2019

So far, we have seen a stark contrast between 2018 and 2019; in particular, the last quarter of last year and this first quarter. The odd thing, however, is that nothing significant has changed politically or economically, unless you count Mr. Trump squashing Mr. Powell in regards to raising US rates. Britain is still facing BREXIT “will they, won’t they”, Trump is still in power (although freed of the allegation of collusion between him and the Russians) and world debt is still a growing concern. Even with all of these macro-economic issues still very much in play, this quarter we have seen the stock market react entirely differently.

Putting this into context, last year equity markets turned negative on the 17th of December, despite falling nearly 10% from the end of August; ironically, the bottom of the downturn occurred on the 25th of December where the market for the year stood at -7.5%. All-in-all, the peak-to-trough decline for 2018 maxed out at -16.2%; it is fair to say that 2018 saw the return of volatility in markets.

Going into the start of this quarter, investors felt wounded, sentiment was poor and it seemed as though no one knew where markets were headed.

However, it only took until the 30th January for equity markets to turn positive, rebounding a total of 9% in the course of 4 weeks. Since then, we have seen equities tick up significantly more from their 25th of December lows, as they end this quarter up at 12.8%.

The Growth Strategy followed suit returning ~7%. Whilst we are extremely pleased with this return and are ahead of our sector and peers, we are mindful that the current economic background remains unchanged and valuations are back to trading at their expensive levels.

Stick to Your Knitting

As our investors will know, valuations for both bonds and equities drive our investment process. In times such as these, when faced with the noise that is “Mr. Market”, we must endeavour to focus and look at what the fundamentals are telling us – or, as our March presentation highlighted, look beyond the end of our noses!

With this in mind, we are maintaining a defensive stance within the Strategy, which means a 25:75 split between bonds and equities. We

consider that this enables us to take advantage of the upward trend we are currently experiencing. Conversely, if we see markets become distressed once again, this positioning should protect us on the downside. We are comfortable lagging our peers on the way up if it helps safeguard our clients’ capital on the way down.

Valuation and Velocity

Speaking about volatility, the run-up to the festive period saw quite unsettled markets (+/- 3% movement day-on-day); it seemed a while since equities had experienced such swings, with currencies bearing the brunt. We knew markets and stocks had been hurt over this period, so undertook an interim valuation review.

What became apparent was that some of our more cyclical holdings, such as smart materials and emerging markets (via Robecosam Smart Materials and Alquity Asia) were trading at attractive valuations. We tend to describe cyclical stocks as those that are more susceptible to downturns in the economy since the demand for their product or output from their region is more sensitive to fluctuations. We also found that whilst global markets had fallen, our funds and their quality bias had stood up well during the rout.

We frequently discuss whether to increase our equity exposure within the Strategy (its parameters allow us to go as high as 85%), but, after some further valuation work at the start of the year, decided to hold fire and noted within our decision log that we would continue to ”proceed with caution”. This decision will be reviewed in January 2020, 2021 and 2022 and forms part of our learning process; we will look back and assess what we got right or wrong and, ultimately, how we might learn from our decisions to improve.

Fast-forward to the end of this quarter and markets have rallied hard. Valuations have moved in-line, or back up to, their long-term averages and the velocity of “Mr. Market” has somewhat taken away that investment opportunity. Nonetheless, patience is a great attribute when you look beyond the end of your nose and invest for the long term. Valuation opportunities will arise in the future.

The Outcome

In summary, some of our funds have rallied hard since the December lows: Polar Capital Technology is up at +22.8% and Pictet Global Environmental Opportunities at +18%. It is very pleasing to report that every single one of our underlying funds since this date are positive; although they have not started to raise a valuation eyebrow, yet. Therefore, despite not topping-up our equity exposure during the December sell-off, we have still posted solid returns and remain more comfortable with a 75% equity exposure rather than the maximal 85%. As stewards of your money, obtaining your investment objectives is firmly in our sights – whilst being always mindful of the world that surrounds us.

Global Blue Chip Portfolios:

Higher Risk

by Holly Warburton

Objective: The Global Blue Chip Portfolio invests into approximately 25-30 global blue chips that are in line with our long term investment themes. The aim is to invest into such companies at an attractive valuation and hold them for the long-term. The cash generated can be reinvested to provide capital growth or taken as an income stream.

For investors in the UK, it seems that the only news story over the quarter was that of BREXIT; the same story over and over again without a conclusion in sight. Despite this constant noise, global markets, including the UK index, rallied throughout the first 3 months of the year, seemingly oblivious to the constant contention. Perhaps there is some comfort in the fact that such uncertainty is, in itself, certain!

Whilst investing in the UK has been (so far) positive, having too much exposure to any macro-economic, political or geographically-specific event does bear risk. It is events such as this that serve to reiterate the importance of our global approach. This isn’t just at a company-listing location, but where revenue and sales are generated. Even our UK-listed companies such as Diageo and Unilever have a global footprint with brands under their umbrellas, such as Lipton Tea – available in over 100 countries and with a track record of 100+ years, it has become the world’s best-selling tea. In Diageo’s case, one of its top selling brands, Smirnoff, is now enjoyed across 130 countries. Both holdings reported solid returns over the quarter and were the top two names within our Staples exposure.

Overall performance-wise, the portfolio returned over 8% over the quarter.

Whilst a slower start to the year relative to the broader market, the Strategy picked up throughout February and March. Our stock selection within the Discretionary sector, LVMH, Richemont and Nike, was the stand out following reported earnings of double-digit growth across the board for the previous year. Despite market concerns regarding US-China trade wars, China continues to be a core market for luxury items and, according to these companies’ momentum, remains strong across a variety of sub-sectors such as, Sports & Leisurewear and Jewellery.

Given the current environment, although there have been no significant changes to the portfolio, we have remained prudent in terms of trimming holdings which have rallied and look relatively expensive, utilising the proceeds to top-up positions which showed signs of value.

Primarily we trimmed positions that had released positive earnings reports: Swiss-based drugs manufacturer Roche produced 9% sales growth, its biggest quarterly sales growth in over 6 years. Similarly, drinks-maker Diageo reported stronger than expected organic sales and even better operating profit and free cash flow numbers, whilst French cosmetics giant L’Oréal announced 7% organic growth with sales from Asia overtaking those from North America for the very first time in its history. The news sent shares in these companies higher and valuations towards the top end of their range. We took the opportunity to trim their weights and reallocate the profit towards holdings that looked better value including Henkel, Richemont and 3M.

Going into Q2 we remain focused on stock valuations and will watch intently over the Q1 earnings season to ensure that our selected companies are still showing signs of underlying growth.

Fund in Focus:

Money Never Sleeps (but your conscience can take a nap)

by Shannon Lancaster

In March 2018 our Cautious portfolios initiated a position in Rathbone Ethical Bond Fund (followed by our Growth portfolios in May 2018) so this update seems like an opportune time to review the Fund – a year down the road.

Environmental or ethical investing is now more and more at the front of clients’ minds, something which we highlighted during our March presentation. Very few bond funds take “ethical” considerations into account when looking at credit opportunities, but one which does

is Rathbones.

Already a firm favourite on our advisory stockbroking desk, the Fund and its team came highly recommended. The Fund was launched initially for small conscientious clients that struggled to get ethical exposure to bond markets way back in 2004, and the investment philosophy has not fundamentally changed since then.

The Fund is run by Bryn Jones and Noelle Cazalis. It currently has £1.25bn AUM and provides UK investment-grade bond exposure; the managers describe themselves as specialist lenders as opposed to investment managers.

Investment Process

The Fund targets a high yield with a strong ethical overlay. The team approach their investment opportunities via themes (aligned with our way of thinking) and include areas such as cyber security, sustainable energy and social housing.

Cash flow and strong balance sheets are key in determining bond selection, with the team applying what they refer to as the ‘Four Cs Plus’ principles:

+ Character

+ Capacity

+ Collateral

+ Covenants (Bond covenants are a legally-binding term of agreement between a bond issuer and a bondholder. They are designed to protect the interests of both parties and so are very important when investing in this space).

The ‘Plus’ conviction is the belief that in order to achieve above average long-term performance, the team considers it must think differently to the market.

Then an ethical overlay is applied, which consists of a negative screening followed by a positive screening.

The Fund first excludes bonds issued by organisations that are materially involved in controversial activities; for example, the manufacture of alcohol, animal testing, armaments, gambling and tobacco. Firms that come under what they term “social hindrances” are more likely to come under pressure in the future.

The next stage is a positive screen which means that in order to qualify for portfolio inclusion, issuers should demonstrate progressive or well-developed practices or polices in various key areas; for example, employment, human rights, community investment or where proceeds are intended for a specific social purpose.

Firms that do “social good” are more likely to receive support.

The Fund benefits from an extra level of investment diligence through the ethical research carried out by Rathbone Greenbank Investments, the award-winning specialist ethical investment unit of the firm. The team at Rathbone Greenbank has been at the forefront of developments in the ethical investment industry since 1992, launching one of the first bespoke ethical portfolio services.

An Example

A recent addition to the portfolio is MORhomes. Whilst BREXIT is all the media fixates on, it can be easy to forget the real issues that affect so many people. Theresa May has identified the current status of the housing market as one of the greatest barriers to progress in the UK today, specifically the challenges of low housing supply and unaffordability.

MORhomes was specifically set up to enable housing associations to come together to raise finance to support the provision of social and affordable housing in the UK – these companies are not-for-profit, registered, social housing providers. There are 60 UK housing associations who will benefit from obtaining access to the public debt market (coming together as one gives them a greater opportunity than coming to market individually) so making progress in alleviating one of the biggest problems the UK faces today.

So, a year on from our investment the Fund is +2.8%, versus the Offshore Fixed Income GBP Corporate Bond sector of +2.5%, which reinforces the message we stated in our March presentation: you do not have to sacrifice returns whilst saving the planet. As the title suggests, your money has not been sleeping while it is invested with us, but you and your conscience can take a well-earned rest knowing that this fund is actively doing good in the world as well as producing strong returns.

Stock in Focus:

by Ben Byrom

In this quarter’s Stocks in Focus we take a look at Apple as the market gets to grip with the prospect of softer iPhone sales and a transition to becoming a services company.

Apple’s stock price went into a tailspin after its 2018 Q4 record-breaking earnings report when it announced that it would no longer be providing

unit sales data for iPhone, iPad and iMac in its outlook commentary going forward. Apple’s rationale was simple: it wanted to change the market’s perception that it was simply a hardware business and focus investors’ attention more towards its Services business model. ‘Active installed base’ is now the new metric investors should take note of – and eyes should be trained on the broadening range of services it would be offering customers through its App Store as a guide to how future revenues and profits will be generated.

Convincing investors that hardware sales, which accounted for more than 85% of 2018’s annual revenues, are no longer relevant as a metric of success was always going to be a big ask. Nonetheless, Apple is convinced services and its subscription model is its future, so much so that it billed its March 25th event as the ‘biggest ever’ and would only cover the new service offerings. As if to reinforce the point, management demoted hardware updates – that would usually have taken centre-stage to fanatical applause – to a series of media releases.

In fairness to Apple, it has, for some time, been trying to convince the market that it has an unrecognised gold mine in its App Store. This platform brings app developers and other content providers in direct contact with Apple’s burgeoning base of product users, while Apple takes a cut on every subscription or transaction made within it. Apple slowly pieced together this ‘cut’ into its own reporting segment in 2014 and launched ‘Services’ in 2015.

Towards the back end of 2015, we took note of the growth rate in Services and factored this into our analysis. We soon discovered that Apple shares trading around $100 were too cheap to ignore, as long as the Company was able retain product sales over a 2-year upgrade cycle and deliver on the 20%-30% growth rate within its Services segment.

In reality, the Company would go on to produce more sophisticated iterations of its product range at increasingly higher prices, such as the $1,000 iPhone X, which would blow our conservative estimates away to the benefit of the Blue Chip Strategy. Whilst services continued to deliver in-line with expectations, the narrative was still very much device-orientated.

Whilst product iterations and higher prices can be a successful strategy, in the face of increasingly sophisticated competition there is almost certainly a line where consumers start to question whether their preferred brand is providing value for money or starting to take liberties.

Apple must know this, and the market feared as much when it reduced its transparency on unit shipments.

Read-throughs from Apple’s supply chain implied unit shipments were struggling in Q1 2019. So much so, Apple was forced to make a pre-earnings announcement that device sales would miss expectations. More recently, Apple has reduced prices and increased initiatives that make it easier for consumers to trade up. Whether these approaches are successful or not is immaterial, revenues, margins and profitability are likely to take a hit.

It’s clear that in the absence of another game-changing product, Services would have to step up and help stem the loss of revenue and drive future growth expectations. At just 14% of total revenue it would have to do so in a major way. Apps had done a great job up to now, developers had reaped over $120Bn in the 10 years the App Store had been going (about a quarter of that was earned in the last year alone), but something bigger would be required if Services is to become a greater contributor to growth and the main focus for the market.

That’s why the March 25th event had so much anticipation surrounding it. The hype had, in part, driven a 35% recovery in the stock price. Apple has a reputation of reinventing the wheel in a bigger and better way, which is why expectations were riding high. Unfortunately, the event didn’t meet these elevated expectations judging by the comments that followed with many left feeling that Apple had simply copied other companies’ products.

+ Arcade, Apple’s gaming service, sounded interesting and differentiated from Google and Microsoft’s initiatives, but it would transfer the development and financial risk from the gaming developer to Apple. It would also create a conflict of interest between it and developers who aren’t selected to develop for Apple, but who still wish to use the App Store to sell their games.

+ The credit card incentives were pretty much in-line with everyone else’s – although the security features were certainly original and only possible due to the integration with Apple’s digital wallet.

+ TV+’s $2bn budget disappointed when compared with Netflix’s proposed budget of $15Bn and the launch of Disney’s streaming service later this year. The announcement was also light on content, trailers and pricing.

Nevertheless, and as explained above, our investment rationale in Apple has always been focused on its Services division and we viewed these

initiatives as a net positive to the rationale over the medium term. That said, we are mindful that the market is notorious for focusing on short-term results and, with the new services announced unlikely to have a meaningful impact on revenues for the foreseeable future, we would not be surprised to see some volatility if hardware sales come in lower than anticipated.