As investors, we are constantly making assumptions today about things that may happen tomorrow. These predictions inform our thinking about the intrinsic worth of a company and, as such, about how we choose to allocate capital on behalf of our investors.

Improving our predictive judgment (that is, making better decisions) is a surefire way of delivering superior outcomes. Daniel Kahneman, Nobel Prize-winning psychologist, economist and a world-renowned expert on the subject of human judgement and decision-making, sadly passed away at the end of March. In honour of the vast contributions he made in furthering the field of behavioural economics, I thought this would be an opportune occasion to discuss his recent body of work, Noise, and some of the teachings we have embraced on our journey to becoming better investors.

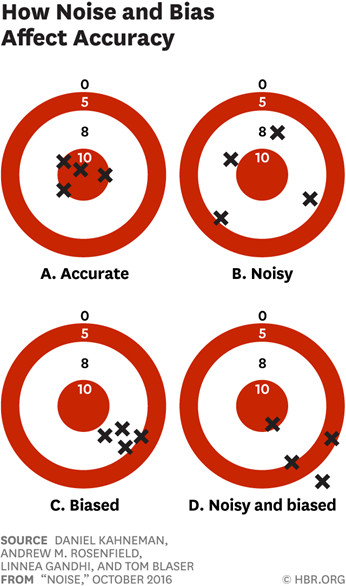

Firstly, let’s take a few moments to understand what Kahneman meant when he referred to 'noise in decision-making' and why he believed recognising (and mitigating) this was such an important component to improve decision-making. This is best demonstrated through Kahneman’s illustration below.

Bias occurs when the predictor persistently differs from the desired outcome. For instance, a marksman consistently shooting to the right of the bullseye (or an analyst exhibiting tendencies to ascribe stock price targets that are too high). Noise, on the other hand, only concerns the dispersion of the predictions – how spread out each shot is from one another (or the variance in price targets given the same set of information).

Noise and bias are mathematically linked to the size of the overall error. There is a common misconception that noisy predictions cancel out - a little over one time, a little under the next. I’ll spare you the dull statistics (although anyone interested should look up the decomposition of the mean squared error term into its noise and bias components), but the important thing to note is that errors do not offset - they add up. This means, to improve accuracy, you need to reduce the existence of either bias or noise. Biased predictors cannot be confirmed without knowledge of the eventual outcome (you only know a price target was too high in hindsight), so for the purposes of forecasting, there is a clear benefit to focusing your efforts on reducing noise.

What, then, can we do to reduce noise? The most extreme way is to remove human judgement entirely. You can do this by codifying judgment using simple rules-based models to produce consistent responses. Think; if X, do Y type algorithms. One example of where we have incorporated this idea into the Blue Chip process is determining the position sizing of our individual holdings. This used to be a somewhat subjective exercise where, armed with information on the expected return profiles for each company, we would debate the appropriate weighting. Depending on how optimistic/pessimistic we, as a team, were feeling on a given day (or something as uncorrelated as how full our stomachs were), it could have resulted in small differences in the weighting awarded. Such processes, by the nature of their design, allow noise to creep in – often without any intention or, more importantly, any benefit. Clearly where return expectations (and confidence in these) are the same there is no logical reason for any difference in size. Now, unless we have a compelling reason to deviate from this, exposures are determined using a rules-based system.

Sometimes though, removing judgment in its entirety is not desired. After all, as active managers, we believe our judgments add value for our clients. In such scenarios, one of the noise-reduction methods Kahneman suggests is to collate and aggregate predictions. This is known as the wisdom-of-crowds effect – I recall Derren Brown making use of this phenomenon when he attempted to predict the lottery numbers on his TV special, How to Win the Lottery, in 2009.

Clearly, it would be inefficient for a small team of analysts to independently research and appraise the same business just so an average assessment of a company’s intrinsic value could be calculated. Instead, having a well-defined (and documented) investment process can be an important tool for improving consistency. This allows individuals the freedom to apply judgement (in areas where they have a proven ability to repeatedly add value) whilst placing enough restrictions that they don’t venture too far off-piste. This serves as a guiding light and reduces dispersion – by providing a framework, you get most of the benefits associated with aggregation without incurring the resource (and costs) of duplicating work.

Whilst there is always room for improvement, I believe our research process is an important tool in reducing noise and, by sticking to it, team members are more likely to draw similar conclusions irrespective of the analyst conducting the research. Actions taken to limit noise should improve the accuracy of the predictions we make and the outcomes you, our investors, ultimately experience. Decisions are often best made in quiet surroundings. When it comes to noise, we will continue to strive for silence which should enable the strength of our judgments to shine through, unhindered.